1-866-840-0279

1-866-840-0279

Many seniors find planning for retirement difficult. While under ideal circumstances you might have saved money throughout your career in preparation for retirement, the reality is that this is often impossible for many people. If you’re approaching the end of your career, or you’re already retired and you’re approaching the end of your existing retirement savings, you may be wondering what alternate funding resources exist.

In this post, we will cover possible untapped revenue streams you might not have realized existed. It’s generally not a good idea to rely on unexpected benefits for your retirement income planning, but in difficult situations, knowing how to find unclaimed retirement benefits can make all the difference in the world. Before you start your search for unclaimed retirement fund benefits, be sure to read through this guide. Or, simply click on one of the links below to jump straight to a category of unclaimed retirement benefits that you think might apply to you.

Social Security benefits

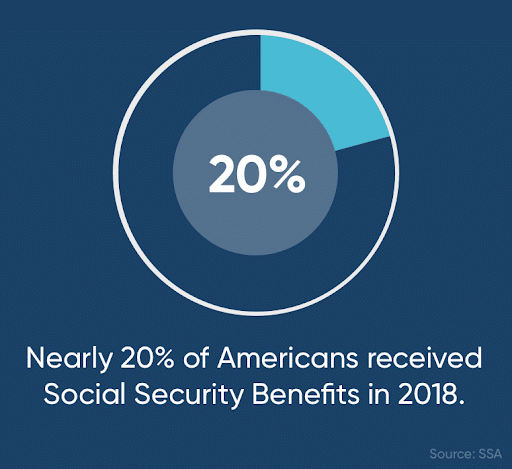

Social Security is one of the most widely used government programs – in 2018 alone, over 62 million Americans received Social Security benefits. Workers qualify for benefits by paying into Social Security during the course of their careers.

Once you turn 62 you may become eligible for Social Security benefits. However, you do actually need to claim them. If you haven’t done so, you may be eligible for unclaimed retirement benefits. How do you know if you qualify?

- You must be over the age of 62

- You must have paid into Social Security during your career

- You must have at least 40 lifetime credits – credits are earned at a rate of up to four per year

- You must fill out an application online, or over the phone by calling 1-800-722-1213

In addition to retirement benefits, Social Security also provides benefits for those with disabilities. If you are disabled and are not collecting any benefits from Social Security, it’s a good idea to apply and see if you can add a revenue stream through this government service. You can also call 1-800-722-1213 to apply.

Those already collecting Social Security benefits and hoping to search for unclaimed retirement benefits from another source might want to check to see if you have unclaimed pension benefits for retirement from previous employers.

Previous employers’ retirement accounts

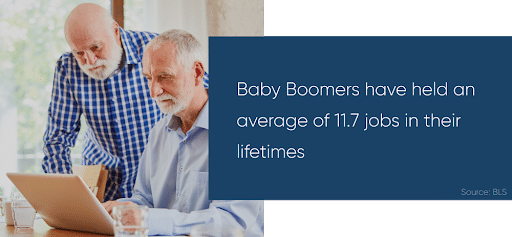

Did you know that Baby Boomers have held an average of 11.7 jobs in their lifetime? Some jobs don’t offer retirement plans, but there’s a chance that at least a few of yours may have. If you’re on the search for unclaimed retirement benefits, it’s worth it to think back on your previous careers and try to recall whether you have claimed your retirement from those employers.

If you suspect that you have money sitting in a retirement account from a previous employer, there are some simple steps you can follow to track it down. Here’s what you can do to find unclaimed retirement benefits, 401ks, or IRAs:

- Contact your old employer. Many HR departments keep detailed information on previous employees, including personal information like retirement accounts held while working at the company. If you have no idea what bank or company might manage your retirement benefits, you can start by calling your old HR to find out who their retirement account partner is.

- Call your retirement account administrator. Once you receive the name of your old account administrator, usually a bank or other financial company, give them a call. They can usually pair you with your old account using information like your name, date of birth, Social Security number, and the employer you worked for when the account was established.

- Check with your state’s unclaimed property officials. If you find that your money is no longer in your retirement account, the next place to look is with your state’s revenue service. In most cases, unclaimed property, including retirement accounts, are turned over to the state government after many years. However, because you are the rightful owner of the funds, it’s usually within your rights to call and ask for them back.

- Rollover your benefits. If you are not retired yet, there is a tax penalty for withdrawing your retirement funds early. To avoid this, roll your benefits over into a different 401k or IRA. You’ll be able to access them without a penalty once you do reach retirement age. If you have already retired, you can simply deposit the discovered funds into whatever account you wish.

If you’ve already rolled over all your previous retirement accounts, the next place that you might want to search for unclaimed retirement benefits is with the IRS.

Insurance benefits

Insurance claims often result in cash payouts. Life insurance policies in particular tend to have larger payouts, so if you are the beneficiary of a deceased family member or close friend, you could have substantial funds available to you. Places to look for unclaimed benefits include:

- Life insurance policies held by deceased loved ones

- Insurance claims from accidents you were involved in

- Health savings accounts from previous medical insurance providers (these can often be rolled over put toward current medical expenses)

In most cases, unclaimed insurance benefits are turned over to the state government after some time. So, if you think you may have been due money years ago but did not claim it at the time, call your state’s revenue service to find out whether the insurance money is still salvageable.

Other unclaimed sources of retirement funding

Knowing how to access unclaimed retirement benefits can increase your stream of revenue in retirement. However, benefits may not be the only type of unclaimed funding available to you. As you look for new sources of cashflow, keep these possibilities in mind.

Unclaimed tax refunds

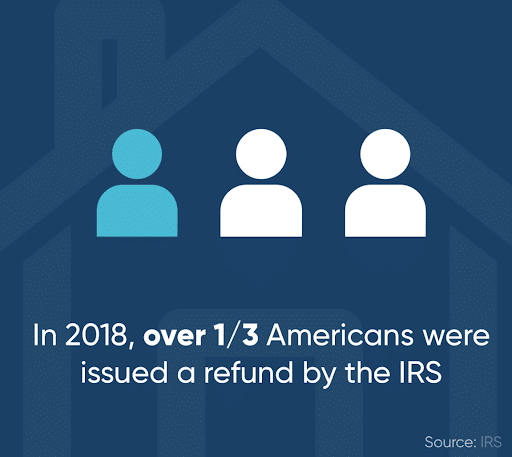

Every year on April 15, Americans are required to fill out and submit a tax return. Tax returns verify the amount that you’ve paid the government in taxes, and also give you an opportunity to claim any credits, deductions, or exemptions that you may qualify for. Because these tax breaks aren’t accounted for on your W-2 form from work, many Americans actually receive refunds on their federal taxes each year. In fact, over 122 million Americans received tax refunds issued by the IRS in 2018.

If you haven’t claimed every tax benefit that’s available to you, you could be missing out on savings. Here are a few of the tax breaks that you might be able to benefit from this coming April:

- The Tax Cuts and Jobs Act nearly doubled the standard deduction starting in 2018. Married couples can deduct $24,000, and $12,000 for single filers. In addition to this benefit, there is an additional deduction of $1,300 for filers over the age of 65.

- While a deduction reduced the amount of income for which you’re taxable, a tax credit is a dollar-for-dollar reduction in the amount that you owe. The Tax Credit for the Elderly or Disabled can help reduce the amount that you owe come tax season. It’s worth between $3,750 and $7,500 depending on circumstances like income and filing status.

- Contributions to IRA accounts are tax deductible, and if you’re over the age of 50, the amount you can contribute increases by $1000 from $6000 to $7000. That means more of the money you add to your accounts is free from taxation – perfect if you’re shoring up your retirement accounts in anticipation of leaving work.

While it might take a while to get your refund, getting an additional break from the government is a great way to access unclaimed funds to put toward retirement. If you’re still looking for places where you might have extra cash stored, check out these next options.

Old bank accounts

Throughout your life, you may find out about new banks offering great interest rates, rewards programs, or investment opportunities. That may cause you to transfer money into that new account – but you might not close out your old account when you transfer. If this sounds plausible, follow these steps to track down your cash:

- Look through old bank statements and emails to find out what banks you have had accounts with.

- Collect personal information like old statements and your Social Security number.

- Call the bank and let them know you think you may still have an account open with them. If you do, they should be able to access it with the help of your information. Once you’ve gained access, simply transfer your remaining funds into your current bank account.

Home equity

Lastly, one often-untapped source of retirement funding is home equity, or the market value of your home minus any standing mortgage or other liens. If you are a home owner and you are retired, you might be eligible for a home equity conversion mortgage, sometimes called a reverse mortgage. These Federal Housing Administration-backed loans allow homeowners to convert the equity in their homes into an additional revenue stream, helping them preserve quality of life while allowing them to age in place.

Reverse mortgage loans are available to seniors who meet certain qualifying conditions:

- You must be at least 62 years old – those with a spouse and co-owner under 62 may also qualify in some cases

- You must own a significant proportion of the equity in your home

- You must occupy the property as your primary residence

These loans can provide a substantial increase in cashflow for seniors, as there are no monthly payments required. Repayment on the loan is not due until a maturation event, like the passing of the borrower. At that point, heirs can either pay off the loan or choose to sell the property.

If you’re interested in a home equity conversion mortgage, a GoodLife representative is always happy to walk you through your options and concerns about reverse mortgage costs. You can also start by trying out the reverse mortgage calculator to see how much money you might be eligible for.

Knowing how to find unclaimed retirement benefits and other sources of funding can be tricky, but by tracking down old accounts, claiming all the government benefits you’re entitled to, and making use of clever financing options, it’s possible to live The GoodLife in Retirement.